.png)

Burial Insurance Terms: Protecting Your Family’s Future

- Lincoln De Freitas

- Dec 24, 2025

- 9 min read

For many Canadian families, planning ahead for end-of-life costs brings peace of mind and real financial security. The reality is that the average funeral in North America can easily exceed $7,000, putting sudden pressure on loved ones at a difficult time. Unlike typical American life insurance, burial insurance is designed specifically to address immediate expenses and lighten your family’s burden. This guide unpacks the essential terms and choices, giving you confidence to make informed, caring decisions.

Table of Contents

Key Takeaways

Point | Details |

Burial Insurance Purpose | Burial insurance offers financial protection for families against unexpected end-of-life expenses, specifically targeting funeral costs and related burdens. |

Policy Types | There are different burial insurance policies, including simplified issue, guaranteed issue, and pre-need plans, each catering to varied health circumstances and financial needs. |

Key Features | Burial insurance features fixed premiums, quick approval processes, and flexible death benefits to ensure accessibility, especially for seniors or those with health issues. |

Common Mistakes | Consumers often misunderstand coverage limitations, overlook alternative options, and fail to compare policies effectively, which can result in inadequate financial protection. |

Defining Burial Insurance Terms and Concepts

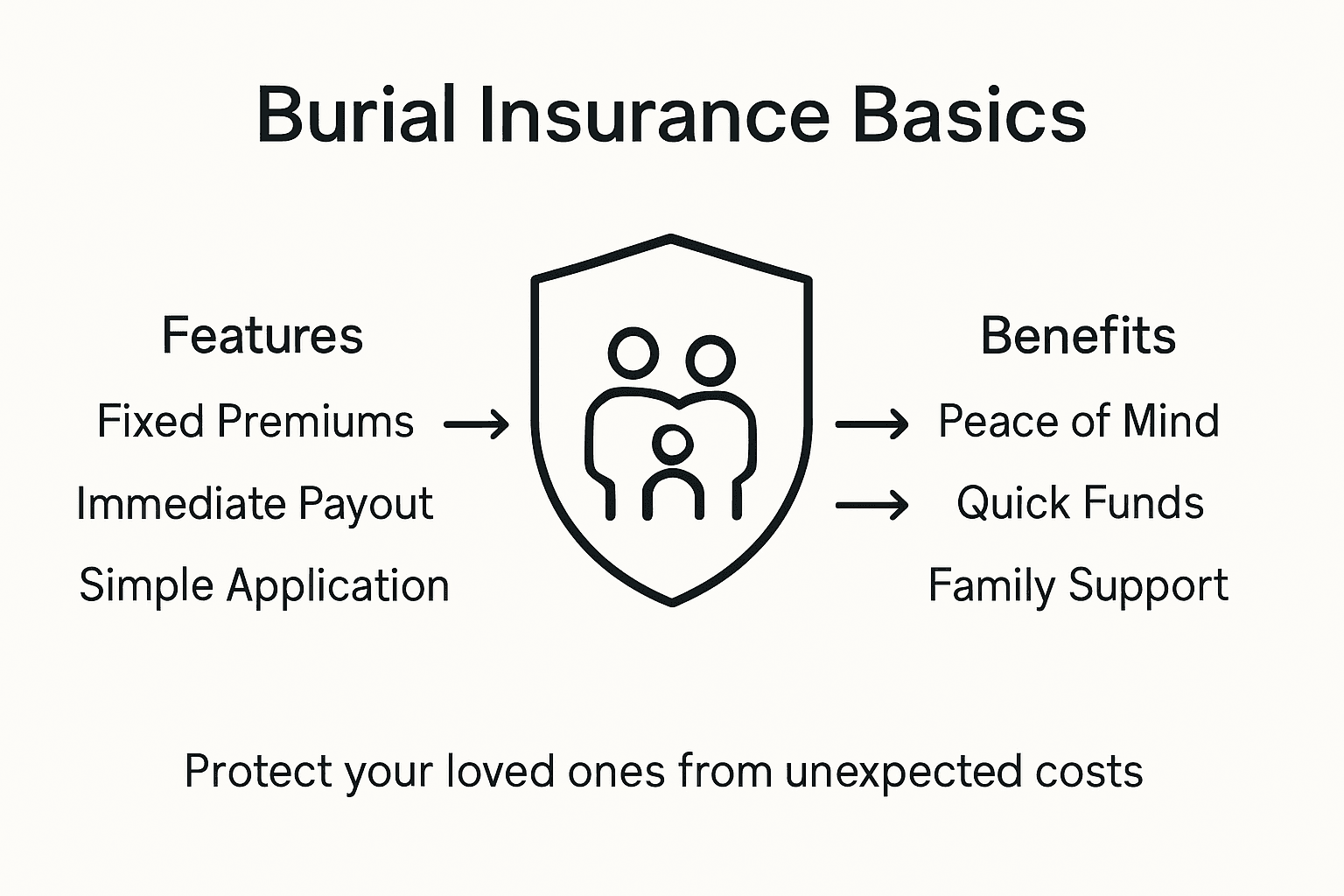

Burial insurance represents a specialized financial protection strategy designed to shield families from unexpected end-of-life expenses. Burial insurance, also known as final expense insurance, provides a targeted solution for covering funeral costs, cremation expenses, and related financial burdens that often overwhelm grieving families.

At its core, burial insurance operates as a specific type of life insurance with unique characteristics. Unlike traditional life insurance policies, these specialized policies typically offer lower coverage amounts, usually ranging from $5,000 to $25,000, and are exclusively focused on managing funeral and memorial service expenses. Key parties involved in a burial insurance contract include the policyholder, the insured individual, designated beneficiaries, and the insurance provider.

The primary purpose of burial insurance is to provide immediate financial relief during a challenging emotional period. Beneficiaries receive a predetermined cash benefit that can be used flexibly for funeral arrangements, outstanding medical bills, or other immediate financial needs. These policies often feature simplified underwriting processes, making them accessible to seniors and individuals who might struggle to qualify for traditional life insurance coverage.

Pro Tip - Financial Planning: Research and compare multiple burial insurance options before selecting a policy, considering factors like premium costs, coverage amounts, and waiting periods to ensure your family’s financial protection.

Key Burial Insurance Terms to Understand:

Beneficiary: The person designated to receive insurance proceeds

Premium: Regular payment required to maintain insurance coverage

Face Value: Total amount payable upon the insured’s death

Waiting Period: Timeframe before full benefits become available

Guaranteed Issue: Policies issued without medical examinations

Types of Burial Insurance Policies Explained

Burial insurance offers multiple policy types designed to meet diverse financial needs and health circumstances. The main types of burial insurance include simplified issue, guaranteed issue, and pre-need funeral plans, each with unique characteristics tailored to different consumer requirements.

Simplified Issue Policies represent a streamlined approach to burial insurance. These policies involve a quick application process with minimal health screening, typically requiring applicants to answer a few basic medical questions. They offer faster approval times and moderate premium rates, making them attractive for individuals with relatively good health who want straightforward coverage without extensive medical examinations.

Guaranteed issue policies provide a critical option for individuals with significant health challenges. These policies accept all applicants regardless of medical history, ensuring coverage accessibility for seniors or those with pre-existing conditions. However, this comprehensive acceptance comes with higher premium costs and often includes waiting periods before full benefits become available. Pre-need funeral plans offer another unique variant, allowing individuals to prepay and prearrange specific funeral services directly with funeral homes, providing both financial and logistical planning.

Key Policy Comparison:

Simplified Issue: Quick approval, limited health questions

Guaranteed Issue: Universal acceptance, higher premiums

Pre-need Plans: Direct funeral service arrangements

Pro Tip - Insurance Selection: Carefully assess your health status, budget, and specific coverage needs before selecting a burial insurance policy to ensure you choose the most appropriate option for your financial situation.

To help clarify the unique options available, here’s a side-by-side comparison of common burial insurance policy types:

Policy Type | Health Requirement | Typical Premiums | Best For |

Simplified Issue | Basic health questions | Moderate | Relatively healthy applicants |

Guaranteed Issue | No health questions | Higher than average | High-risk or older applicants |

Pre-need Funeral Plan | Direct with funeral home | Varies by service | Those preferring prepaid plans |

Key Policy Features and How They Work

Burial insurance policies come with distinctive characteristics designed to simplify end-of-life financial planning. Key features include fixed premiums, straightforward death benefits, and typically no requirement for medical examinations, making these policies uniquely accessible for seniors and individuals with complex health backgrounds.

Fixed Premiums represent a crucial aspect of burial insurance policies. These rates remain constant throughout the policy’s lifetime, providing predictable financial planning for policyholders. Unlike traditional life insurance with variable rates, burial insurance ensures that monthly payments remain unchanged, protecting consumers from unexpected cost increases. This stability allows individuals to budget effectively and maintain continuous coverage without financial strain.

The death benefit in burial insurance is specifically structured to cover immediate end-of-life expenses. Beneficiaries receive a predetermined cash amount typically ranging from $5,000 to $25,000, which can be used flexibly for funeral costs, outstanding medical bills, or other immediate financial needs. This targeted approach distinguishes burial insurance from broader life insurance policies, focusing specifically on managing the financial challenges associated with a loved one’s passing.

Key Policy Features Breakdown:

No Medical Exam: Simplified application process

Fixed Premiums: Consistent monthly payments

Flexible Death Benefit: Funds usable for various expenses

Quick Approval: Faster processing compared to traditional policies

Guaranteed Acceptance: Options for individuals with health challenges

Pro Tip - Financial Protection: Review your policy’s specific terms carefully, paying special attention to waiting periods and coverage limitations to ensure comprehensive end-of-life financial planning.

Understanding Eligibility and Application Process

The application process for burial insurance varies significantly depending on policy type, creating multiple pathways for individuals seeking end-of-life financial protection. Different policy approaches accommodate various health backgrounds, age ranges, and personal circumstances, ensuring accessibility for most consumers.

Simplified Issue Policies represent the most common application route. These policies require applicants to complete a brief health questionnaire, typically covering basic medical history, recent diagnoses, and lifestyle factors. While not requiring a full medical examination, these policies do involve some health screening. Applicants with relatively good health can expect faster approval times and potentially lower premium rates. The questionnaire helps insurers assess risk quickly, allowing for streamlined decision-making.

Guaranteed issue policies offer a critical alternative for individuals with complex health histories or those who might not qualify for traditional insurance. These policies accept all applicants regardless of medical condition, providing a universal coverage option. The trade-off for this comprehensive accessibility is typically higher premium costs and potentially longer waiting periods before full benefits become available. Some guaranteed issue policies may include graded death benefits, where the full payout is only accessible after a specific waiting period.

Application Process Steps:

Gather Personal Information: Social security number, contact details

Complete Health Questionnaire: For simplified issue policies

Select Coverage Amount: Typically $5,000 to $25,000

Choose Beneficiary: Designate who receives the death benefit

Review Policy Terms: Understand waiting periods and exclusions

Pro Tip - Application Preparation: Collect all medical and personal documentation in advance to expedite the application process and increase your chances of quick approval.

Costs, Payouts, and Financial Implications

Burial insurance policies typically offer death benefits ranging from $5,000 to $25,000, designed to cover funeral and related end-of-life expenses. These specialized insurance products provide a targeted financial solution for families facing unexpected funeral costs, ensuring minimal financial burden during an emotionally challenging time.

Premium Structures play a critical role in burial insurance affordability. Premiums can start as low as $62 per month for coverage amounts between $5,000 and $40,000, with costs varying based on factors such as age, gender, health status, and selected coverage amount. Younger and healthier applicants typically receive more favorable rates, while older individuals or those with complex medical histories might encounter higher monthly payments. Consumers can choose between monthly or annual payment options, providing flexibility in financial planning.

The death benefit in burial insurance serves as a crucial financial safety net for beneficiaries. Unlike traditional life insurance, these policies focus specifically on immediate end-of-life expenses. Beneficiaries receive a predetermined cash amount that can be used flexibly for funeral services, outstanding medical bills, cremation costs, or other immediate financial needs. This targeted approach ensures that families are not overwhelmed by sudden expenses during their grieving period, offering both financial and emotional support.

Financial Considerations:

Coverage Range: $5,000 to $25,000 typical benefit

Premium Factors: Age, health, gender

Payment Options: Monthly or annual

Benefit Flexibility: Funds usable for multiple expenses

No Medical Exam: Simplified qualification process

Pro Tip - Financial Planning: Compare multiple insurance providers and carefully review policy terms to find the most cost-effective burial insurance that meets your specific financial protection needs.

The following table summarizes important financial factors to consider before selecting a burial insurance policy:

Financial Factor | Why It Matters | Typical Range or Impact |

Coverage Amount | Determines payout | $5,000 - $25,000 |

Premium Cost | Affects affordability | $62/month and up, age dependent |

Waiting Period | Delays full benefit payout | 0-2 years, varies by policy |

Payment Options | Allows budgeting flexibility | Monthly or annual |

Common Misconceptions and Mistakes to Avoid

Many consumers mistakenly believe burial insurance is the only option for covering funeral expenses, overlooking alternative financial strategies for end-of-life planning. Understanding these misconceptions can help individuals make more informed decisions about their financial protection and legacy planning.

Coverage Limitations represent a critical area of misunderstanding. Burial insurance policies typically offer lower coverage amounts compared to traditional life insurance, which can lead to unexpected financial gaps. Some policyholders assume these policies will cover all end-of-life expenses, but coverage is often limited and may not fully address all potential costs. Premiums can be significantly higher for older applicants, and many policies include waiting periods before full death benefits become accessible, creating potential financial risks for families.

Another common mistake involves failing to compare multiple insurance options comprehensively. Consumers often select the first policy they encounter without thoroughly evaluating different providers, coverage terms, and potential alternatives. This approach can result in suboptimal financial protection, higher-than-necessary premiums, or inadequate coverage for specific family needs. Careful research and comparison are essential to finding the most appropriate burial insurance solution.

Key Misconception Warning Signs:

Assuming Universal Coverage: Not all policies cover complete funeral expenses

Ignoring Waiting Periods: Some policies delay full benefit payouts

Overlooking Alternative Options: Other insurance types might be more suitable

Disregarding Premium Variations: Costs can differ significantly between providers

Failing to Read Fine Print: Critical limitations may be hidden in policy details

Pro Tip - Strategic Planning: Consult with a licensed insurance professional who can provide personalized guidance tailored to your specific financial circumstances and family protection needs.

Secure Your Family’s Future with Trusted Burial Insurance Solutions

Understanding burial insurance terms like beneficiary, premium, and waiting period is the first step to protecting your loved ones from unexpected end-of-life expenses. If you want clear, compassionate guidance on choosing the right final expense insurance, LD Financial Services offers personalized support that respects your unique situation. Our solutions include guaranteed issue and simplified application policies with fixed premiums designed to provide peace of mind when it matters most.

Don’t wait until it’s too late. Visit LD Financial Services today to explore affordable burial insurance options tailored for middle-aged and senior adults. Book a consultation with our licensed agents now to secure a plan that ensures your family’s financial protection and legacy are honored without the stress. Learn more about how we simplify the process and keep your coverage accessible and dependable for the future.

Frequently Asked Questions

What is burial insurance?

Burial insurance, also known as final expense insurance, is a type of life insurance designed to cover funeral costs and related expenses, providing financial protection for families during difficult times.

What are the main types of burial insurance policies?

The main types of burial insurance include simplified issue policies, which require minimal health questions; guaranteed issue policies, which accept all applicants regardless of health; and pre-need funeral plans, allowing individuals to arrange and pay for specific funeral services in advance.

How do burial insurance premiums work?

Burial insurance premiums are regular payments made to maintain coverage. They vary based on factors like age, health status, and the selected coverage amount. Many policies feature fixed premiums, allowing for predictable financial planning.

What should I consider when choosing a burial insurance policy?

When selecting a burial insurance policy, consider factors such as premium costs, coverage amounts, waiting periods for benefits, and specific terms of the policy, ensuring it aligns with your financial protection needs.

Recommended