.png)

Difference Between Term and Whole Life – Impact on Legacy

- Lincoln De Freitas

- a few seconds ago

- 8 min read

Most American families face tough choices when deciding how to protect loved ones from unexpected expenses and future uncertainties. As health needs become more complex with age, picking the right life insurance can shape your family’s financial future. This guide explains the key differences between term and whole life insurance, helping you understand which option best supports your peace of mind and protects your family—especially when studies show that over 60 percent of Americans say life insurance is essential for financial security.

Table of Contents

Key Takeaways

Point | Details |

Understanding Insurance Types | Term life insurance offers affordable, temporary coverage, while whole life insurance provides lifelong protection with cash value accumulation. |

Financial Planning Considerations | Evaluate your financial goals and family needs when choosing between term and whole life insurance for the best fit. |

Premium and Cost Differences | Term life has lower initial premiums with potential increases upon renewal, whereas whole life features higher fixed premiums over the policyholder’s lifetime. |

Suitability Based on Life Stage | Young families typically benefit from term life, while whole life is ideal for those seeking long-term financial security and legacy planning. |

Defining Term and Whole Life Insurance

Life insurance represents a critical financial planning tool designed to provide financial protection for your loved ones. At its core, two primary types of life insurance dominate the market: term life insurance and whole life insurance, each offering distinct features and benefits tailored to different financial goals.

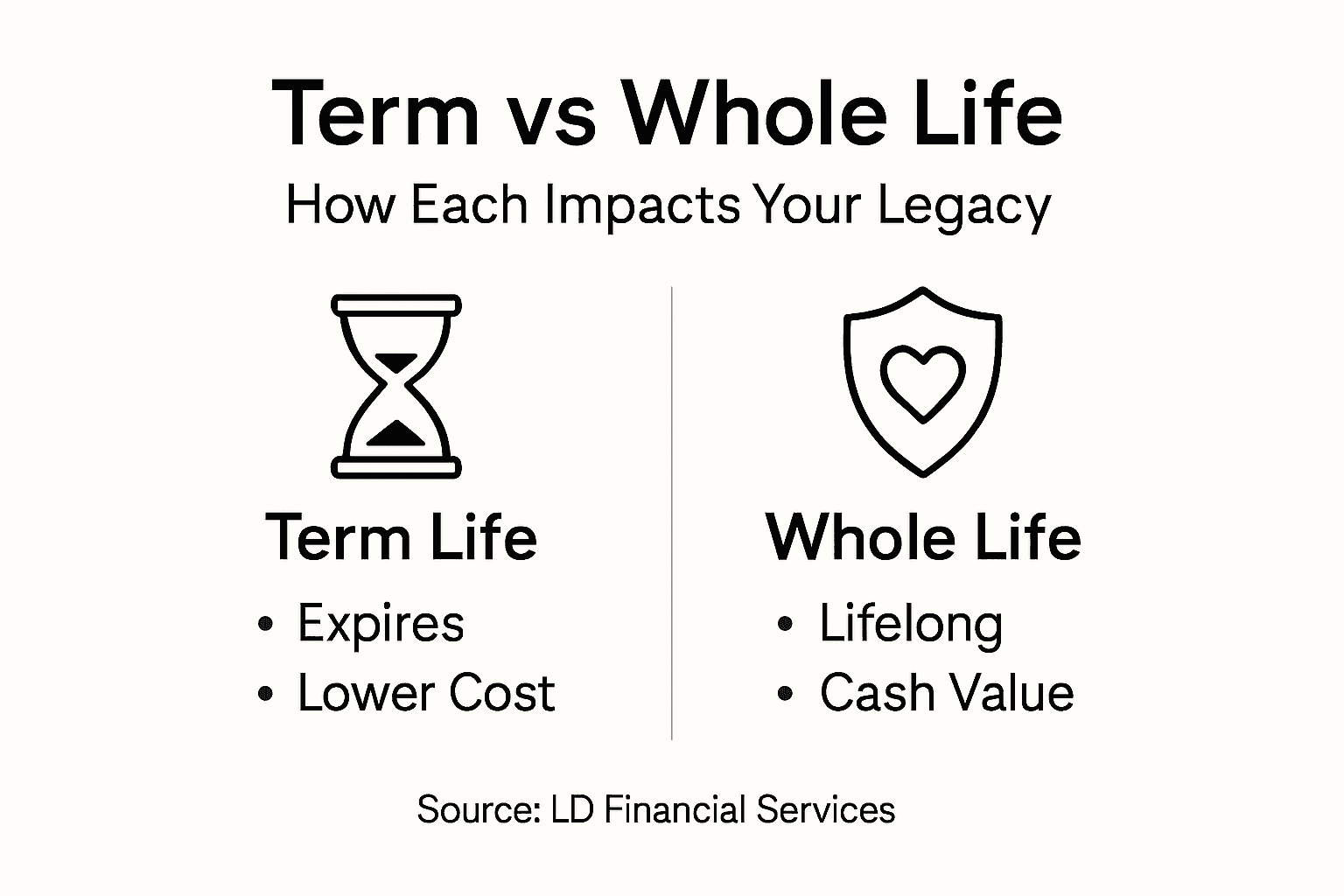

Term life insurance provides coverage for a specific period, typically ranging from 10 to 30 years, and is generally more affordable. Insurance coverage periods can include 1, 5, 10, or 20-year terms with a straightforward death benefit paid only if the policyholder passes away during the contracted timeframe. This type of insurance acts like a financial safety net, ensuring your family receives monetary support if you die unexpectedly during the policy’s active period.

In contrast, whole life insurance offers lifelong coverage with a guaranteed death benefit and a unique cash value component that accumulates over time. Unlike term policies, whole life insurance provides permanent protection and builds a tax-advantaged savings plan alongside the death benefit. Policyholders can borrow against the accumulated cash value, offering financial flexibility that term life insurance cannot match. Whole life insurance benefits extend beyond simple protection, functioning as a potential investment vehicle with guaranteed growth.

Pro tip: Consider your specific financial situation, long-term goals, and family needs when selecting between term and whole life insurance, as each policy type offers unique advantages tailored to different life stages.

Here’s a concise comparison of term and whole life insurance for easy reference:

Aspect | Term Life Insurance | Whole Life Insurance |

Coverage Duration | 10–30 years, specified | Permanent, lifelong |

Cash Value | No built-in savings | Accumulates over time |

Premium Structure | Low, may increase on renewal | Fixed, higher upfront cost |

Policy Flexibility | Can be renewed/converted | May offer loans/dividends |

Key Features and Coverage Options

Understanding the nuanced features of term and whole life insurance requires a comprehensive examination of their distinct coverage options. Coverage types vary significantly between these two primary life insurance approaches, with each offering unique benefits tailored to different financial planning strategies.

Term life insurance delivers straightforward protection with key features that prioritize affordability and simplicity. Insurance coverage variations include fixed periods ranging from 10 to 30 years, providing a clear financial safety net during critical life stages. These policies are characterized by lower premium costs and a direct death benefit, making them attractive for individuals seeking maximum coverage at minimal expense. Typical term life features include:

Predetermined coverage periods

Lower premium rates

Simple, no-frills protection

Renewable and convertible options in many policies

Whole life insurance, by contrast, offers a more comprehensive financial instrument with robust features extending beyond basic death benefit protection. These policies integrate lifelong coverage with a growing cash value component that functions as a potential investment vehicle. Policyholders can access accumulated cash value through loans or withdrawals, providing financial flexibility not available in term life policies. Key whole life insurance features encompass:

Guaranteed lifelong coverage

Cash value accumulation

Fixed premium structures

Potential dividend payments

Option to borrow against policy value

Pro tip: Carefully evaluate your long-term financial goals and current life stage to determine which policy features align most closely with your personal and family financial needs.

Premiums, Costs, and Payout Structures

Life insurance premiums represent a critical financial consideration that dramatically impacts long-term planning and family protection strategies. Insurance premium structures reveal significant differences between term and whole life insurance policies, with each approach offering unique cost implications for policyholders.

Term life insurance stands out as the more affordable option, particularly for younger individuals seeking substantial coverage at minimal expense. These policies typically feature lower initial premiums that remain consistent during the selected term period. However, renewal rates can increase substantially as the policyholder ages, potentially making long-term affordability challenging. Key premium characteristics include:

Lower initial cost

Premiums based on age and health at policy inception

Limited coverage duration

Potential rate increases upon renewal

Whole life insurance presents a more complex financial instrument with higher upfront premiums that remain fixed throughout the policyholder’s lifetime. Permanent life insurance costs reflect the policy’s dual nature as both protection and potential investment vehicle. These premiums incorporate:

Guaranteed lifelong coverage

Cash value accumulation

Level premium structure

Mortality and administrative costs

Potential dividend distributions

Payout structures for both policy types ultimately provide tax-free death benefits to designated beneficiaries. Term life policies pay out only if death occurs during the specific contract period, while whole life policies guarantee payment regardless of when the policyholder passes away. The key difference lies in the additional cash value component of whole life insurance, which allows policyholders to potentially access funds during their lifetime.

Pro tip: Calculate your long-term financial needs and compare premium costs across multiple policy types to identify the most cost-effective protection strategy for your specific life circumstances.

Benefits for End-of-Life Planning

End-of-life planning represents a critical financial strategy that goes far beyond simple insurance coverage. Medicaid insurance considerations reveal nuanced implications for different life insurance approaches, particularly when managing long-term care and estate planning needs.

Term life insurance offers significant advantages for individuals seeking targeted financial protection during specific life stages. These policies provide essential benefits for end-of-life planning, including:

Affordable coverage during high-risk periods

Financial protection for dependent family members

Flexibility to match specific financial obligations

Temporary safety net for mortgage or child-rearing expenses

Quick and straightforward claim processes

Whole life insurance emerges as a more comprehensive solution for individuals seeking permanent financial protection and legacy planning. Unlike term policies, whole life insurance integrates multiple end-of-life planning benefits:

Guaranteed lifelong coverage

Cash value accumulation for unexpected expenses

Potential tax-advantaged asset transfer

Ability to access funds during policyholder’s lifetime

Stable financial planning instrument

The critical distinction lies in how these policies interact with broader financial planning strategies. Term life insurance provides immediate, cost-effective protection, while whole life insurance offers a more nuanced approach to long-term financial security. Families can strategically combine these options to create a robust end-of-life financial strategy that addresses immediate needs and future uncertainties.

Pro tip: Consult a financial advisor to develop a personalized insurance strategy that aligns with your specific family circumstances and long-term financial goals.

Choosing the Right Policy for Your Needs

Selecting the appropriate life insurance policy requires careful consideration of your unique financial landscape and long-term objectives. Policy selection strategies involve analyzing multiple factors that determine the most suitable coverage for your individual circumstances.

For younger adults and families with specific financial protection needs, term life insurance often emerges as the most strategic choice. Ideal candidates for term policies typically include:

Young parents with dependent children

Individuals with significant mortgage obligations

People seeking maximum coverage at minimal cost

Those with temporary financial protection requirements

Professionals in high-risk career fields

Whole life insurance represents a more comprehensive solution for individuals prioritizing lifelong financial security and legacy planning. Optimal candidates for whole life policies generally include:

High-net-worth individuals

Those seeking permanent estate planning tools

Individuals with long-term financial dependents

People interested in tax-advantaged wealth transfer

Those wanting guaranteed cash value accumulation

The decision between term and whole life insurance ultimately depends on your specific financial goals, risk tolerance, and family dynamics. Careful evaluation of your current financial situation, future obligations, and long-term objectives will guide you toward the most appropriate insurance strategy. Consider consulting a financial professional who can provide personalized guidance tailored to your unique circumstances.

Pro tip: Review your life insurance needs every 3-5 years or after major life events to ensure your policy continues to align with your evolving financial landscape.

Consider these policy selection factors to match insurance with your financial goals:

Factor | Term Life Best For | Whole Life Best For |

Budget Constraints | Limited, cost-focused plans | Willing to pay for investment growth |

Financial Planning Horizon | Short- to medium-term needs | Long-term wealth transfer and planning |

Desire for Investment | Pure protection focus | Savings and estate building |

Family Dependency | Temporary obligations | Lifelong dependents or legacy wishes |

Secure Your Legacy with the Right Life Insurance Choice

Choosing between term and whole life insurance can feel overwhelming, especially when it comes to protecting your family and managing end-of-life expenses. The article highlights key challenges such as balancing affordable premiums with lifelong financial security and creating a legacy that covers funeral costs, medical bills, and other outstanding debts. Whether you need temporary coverage that fits your current budget or permanent protection that builds cash value, understanding these options is crucial for peace of mind.

At LD Financial Services, we specialize in final expense insurance solutions designed to ease these worries. Our compassionate approach offers clear, affordable plans including guaranteed issue life insurance and permanent policies with fixed premiums and simplified applications. You can trust us to help you secure a policy tailored to your unique needs so your loved ones are protected without the burden of unexpected costs.

Ready to take control of your financial legacy today? Explore our final expense insurance solutions to find the coverage that fits your goals.

Contact one of our licensed agents now for a free consultation. Protect your family and leave a lasting legacy by starting your application at LD Financial Services.

Frequently Asked Questions

What is the main difference between term and whole life insurance?

Term life insurance provides coverage for a specified period, typically 10 to 30 years, while whole life insurance offers lifelong coverage with a cash value component that accumulates over time.

How do the costs differ between term and whole life insurance?

Term life insurance generally has lower initial premiums that may increase upon renewal, while whole life insurance has higher fixed premiums that remain consistent throughout the policyholder’s lifetime due to its cash value feature.

How does each type of life insurance impact legacy planning?

Whole life insurance is better suited for legacy planning because it guarantees lifelong coverage and includes a cash value that can be leveraged for estate planning. Term life insurance provides temporary protection but does not accumulate cash value, making it less effective for long-term legacy goals.

Can I convert my term life insurance policy to whole life insurance?

Many term life insurance policies offer conversion options that allow policyholders to convert their term coverage to whole life insurance before the term ends, providing flexibility as financial needs change.

Recommended