.png)

End-of-Life Insurance Options: Protecting Family Finances

- Lincoln De Freitas

- Jan 2

- 9 min read

More than half of Canadian seniors worry their families could face overwhelming expenses after they are gone, a concern shared by many American families as well. As health challenges become part of everyday life, understanding end-of-life insurance can feel confusing and intimidating. This guide offers clear answers on policy types, costs, and common mistakes, helping you protect your loved ones from financial hardship when it matters most.

Table of Contents

Key Takeaways

Point | Details |

Understanding End-of-Life Insurance | These policies provide financial support for families to cover immediate post-death expenses, focusing on easing financial burden during grief. |

Types of Policies | Guaranteed issue, term, and permanent life insurance each serve different needs, varying in cost, coverage, and application processes. |

Importance of Coverage Assessment | Properly evaluating anticipated expenses ensures adequate coverage, preventing families from facing financial strain later. |

Thorough Policy Review | Consumers should carefully examine policy terms and conditions to avoid unexpected complications and ensure comprehensive protection. |

Defining End-of-Life Insurance Policies

End-of-life insurance represents a specialized financial protection mechanism designed to provide critical support for families during challenging times. Life insurance policies specifically crafted for end-of-life expenses are financial instruments that guarantee monetary support to beneficiaries following an individual’s passing.

These policies differ significantly from traditional life insurance by focusing exclusively on covering immediate post-death financial responsibilities. Typical end-of-life insurance coverage includes funeral expenses, outstanding medical bills, legal settlement costs, and potential remaining personal debts. The primary objective is ensuring families are not burdened with substantial financial strain during their period of grief and emotional vulnerability.

Most end-of-life insurance policies offer streamlined qualification processes compared to standard life insurance products. These policies are designed to provide quick financial assistance to beneficiaries, often with minimal medical underwriting and accelerated approval timelines. This approach makes such insurance more accessible for seniors or individuals with complex medical histories who might struggle to obtain traditional life insurance coverage.

Pro tip: Research and compare multiple end-of-life insurance options, considering factors like coverage amount, premium costs, and specific policy exclusions to find the most suitable protection for your family’s unique financial needs.

Comparing Types: Guaranteed Issue, Term, Permanent

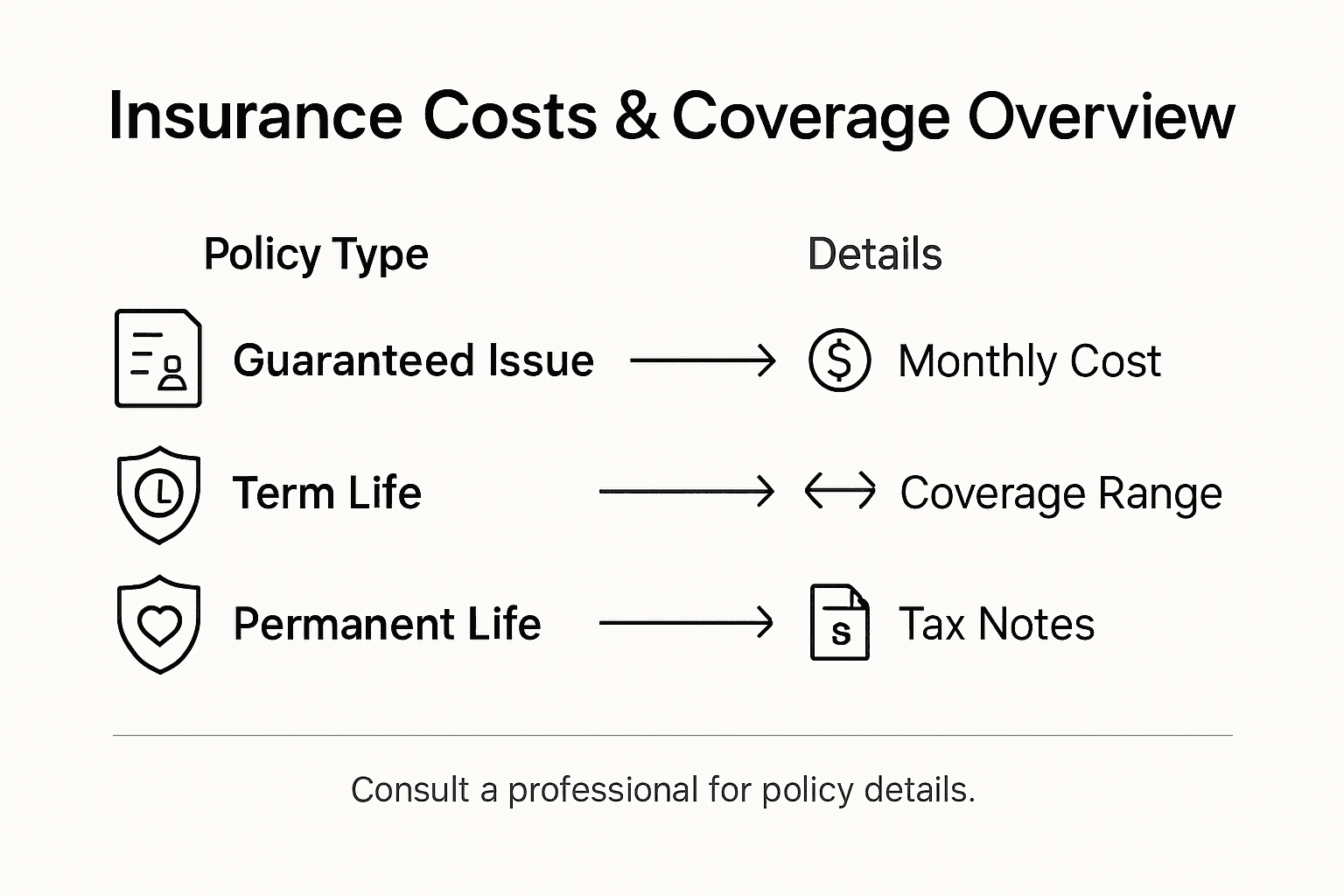

End-of-life insurance offers multiple policy types, each with unique characteristics designed to meet different financial protection needs. Guaranteed issue, term, and permanent insurance represent the primary categories of life insurance for end-of-life planning, each presenting distinct advantages and considerations for potential policyholders.

Guaranteed Issue Policies provide immediate coverage without medical examinations, making them ideal for individuals with complex health histories. These policies typically feature higher premiums and lower coverage amounts due to the reduced underwriting requirements. They guarantee acceptance regardless of health status, ensuring that seniors or those with pre-existing conditions can secure financial protection for their families.

Term Life Insurance offers coverage for a specific period, usually ranging from 10 to 30 years. These policies provide straightforward protection with lower initial costs but require careful timing to ensure comprehensive end-of-life financial coverage. If the policyholder passes away during the designated term, beneficiaries receive the full benefit. However, if death occurs after the term expires, no benefits are paid, potentially leaving families financially vulnerable.

Permanent Life Insurance delivers lifelong coverage with additional benefits like cash value accumulation. Whole life and universal life variations provide consistent protection and potential investment opportunities. While more expensive than term policies, permanent insurance ensures your beneficiaries receive support regardless of when death occurs, offering comprehensive and predictable financial planning.

Here’s a side-by-side summary to help compare key end-of-life insurance types:

Insurance Type | Best For | Coverage Amounts | Main Application Requirement |

Guaranteed Issue | Seniors, poor health | $5,000–$25,000 | Basic info, age verification |

Term Life | Young, healthy adults | $50,000–$500,000 | Health exam, medical review |

Permanent Life | Long-term planners | Varies, often $50,000+ | Comprehensive medical underwriting |

Pro tip: Consult a financial advisor to assess your specific health, age, and financial circumstances before selecting an end-of-life insurance policy to ensure optimal coverage and cost-effectiveness.

Features and Benefits of Each Policy

End-of-life insurance policies offer unique features designed to address diverse financial protection needs. Understanding the distinctive characteristics of each policy type helps individuals make informed decisions that align with their specific financial circumstances and family protection goals.

Guaranteed Issue Policies present several compelling advantages for individuals facing health challenges. These policies eliminate medical examinations and health screenings, providing automatic acceptance regardless of medical history. Key features include simplified application processes, immediate coverage, and guaranteed approval. However, these benefits come with trade-offs: higher premium rates and typically lower maximum coverage amounts compared to traditional life insurance products. They serve as a critical safety net for seniors or individuals with pre-existing medical conditions who might otherwise struggle to secure financial protection.

Term Life Insurance offers cost-effective coverage with straightforward benefits. Policies are structured around specific timeframes, typically ranging from 10 to 30 years, with predictable premium structures. The primary advantages include lower initial costs, flexibility in coverage duration, and substantial death benefits if the policyholder passes away during the designated term. These policies provide a balanced approach to financial protection, allowing individuals to secure coverage during critical life stages such as mortgage payments, child-rearing years, or specific financial obligations.

Permanent Life Insurance delivers comprehensive, lifelong financial protection with additional investment components. Whole life and universal life variations offer guaranteed death benefits, consistent premium structures, and a unique cash value accumulation feature. Policyholders can potentially borrow against the policy’s cash value or use it as a supplemental retirement planning tool. Unlike term policies, permanent insurance ensures continuous coverage, providing families with long-term financial security and potential financial flexibility.

Pro tip: Request detailed policy illustrations from multiple insurance providers to compare exact coverage amounts, premium structures, and potential cash value growth before making a final decision.

Eligibility Requirements and Application Process

End-of-life insurance application processes vary significantly across different policy types, presenting unique challenges and opportunities for potential policyholders seeking financial protection.

Guaranteed Issue Policies represent the most accessible insurance option, designed for individuals with complex medical histories or health challenges. These policies feature minimal eligibility requirements, typically requiring only basic personal information and age verification. No medical examinations or extensive health screenings are conducted, ensuring almost universal acceptance. The streamlined application process allows seniors and individuals with pre-existing conditions to secure coverage quickly, though this convenience comes with higher premium rates and lower maximum benefit amounts.

Term and Permanent Life Insurance applications involve more comprehensive evaluation processes. Applicants must complete detailed health questionnaires and potentially undergo medical examinations to determine risk and premium structures. Insurance providers typically review medical records, conduct blood tests, and assess overall health status. Factors such as age, medical history, lifestyle choices, and current health conditions directly impact eligibility and pricing. Younger, healthier applicants generally receive more favorable terms, with lower premiums and higher potential coverage amounts.

The application timeline can vary depending on the policy type and individual circumstances. Guaranteed issue policies often provide near-instant approval, while term and permanent insurance applications may take several weeks to process. Applicants should prepare comprehensive medical documentation, including physician contact information, recent medical test results, and a detailed health history. Some insurers may require additional documentation or follow-up medical consultations to complete the underwriting process.

Pro tip: Gather all medical records, prescription histories, and relevant health documentation before starting the application process to expedite approval and improve your chances of securing favorable insurance terms.

Costs, Coverage Amounts, and Tax Implications

Insurance costs and coverage amounts vary significantly across different end-of-life policy types, requiring careful financial planning and strategic decision-making for potential policyholders.

Guaranteed Issue Policies typically feature higher premium rates relative to coverage amounts. These policies compensate for their simplified approval process by charging elevated prices, usually ranging from $50 to $300 monthly depending on the policyholder’s age and desired benefit level. Coverage amounts are generally more limited, often between $5,000 and $25,000, making them suitable for covering basic funeral expenses and immediate end-of-life financial obligations. The trade-off for accessibility is higher per-dollar costs compared to more traditional insurance options.

Term Life Insurance offers more cost-effective coverage with substantial benefit amounts during specific timeframes. Premiums are typically lower and coverage amounts can range from $50,000 to $500,000, depending on the policyholder’s health, age, and selected term length. Monthly costs can be as low as $20 for younger, healthier individuals, making these policies attractive for targeted financial protection during critical life stages such as mortgage payments or child-rearing years. However, once the term expires, no benefits are payable, creating potential coverage gaps.

Permanent Life Insurance represents the most comprehensive but expensive option, with premiums reflecting lifelong coverage and additional cash value accumulation. These policies often include tax-advantaged investment components, allowing policyholders to build financial reserves while maintaining insurance protection. Death benefits are generally paid tax-free to beneficiaries, though complex ownership structures might trigger estate tax considerations. Policyholders can potentially borrow against accumulated cash value, providing financial flexibility beyond traditional insurance protection.

Here’s a quick reference on costs, tax impacts, and policy flexibility:

Policy Type | Typical Monthly Cost | Tax Considerations | Policy Flexibility |

Guaranteed Issue | $50–$300 | Death benefit tax-free | Minimal flexibility |

Term Life | $20+ (varies by age/term) | Death benefit tax-free | Renewable or convertible terms |

Permanent Life | Higher ($100+ typical) | Cash value may grow tax-deferred | Loans/withdrawals allowed |

Pro tip: Consult a tax professional to understand the specific tax implications of your life insurance policy, as ownership structure and premium payment strategies can significantly impact potential tax consequences.

Mistakes to Avoid When Choosing a Policy

Selecting an end-of-life insurance policy requires careful consideration to prevent costly long-term financial mistakes, with numerous potential pitfalls that can compromise family financial protection.

Inadequate Coverage Assessment represents a critical error many individuals make when choosing insurance. Many policyholders underestimate their actual financial needs, selecting coverage amounts insufficient to address funeral expenses, outstanding debts, and potential medical bills. This miscalculation can leave families financially vulnerable during an already emotionally challenging period. Consumers should conduct a comprehensive financial review, calculating exact anticipated expenses and potential future obligations to determine appropriate coverage levels.

Overlooking Policy Details can lead to unexpected complications and financial disappointments. Consumers frequently make mistakes by not thoroughly understanding policy terms, exclusions, waiting periods, and potential premium increases. Some policies include specific conditions that might limit payouts or require complex qualification processes. Common oversights include ignoring clauses about pre-existing conditions, failing to understand how health changes might impact coverage, and not recognizing potential restrictions on benefit payments.

Another significant mistake involves selecting policies based solely on price without considering long-term financial implications. Cheaper policies might seem attractive initially but can prove substantially more expensive over time due to limited coverage, higher future premium increases, or restrictive terms. Individuals should evaluate policies holistically, considering factors like financial stability of the insurance provider, comprehensive coverage options, flexibility in policy terms, and potential cash value accumulation for permanent insurance types.

Pro tip: Request and carefully review multiple policy illustrations from different providers, comparing not just initial costs but total projected expenses and coverage details over your expected policy duration.

Secure Your Family’s Financial Future with Trusted End-of-Life Insurance

Facing the challenge of selecting the right end-of-life insurance can feel overwhelming. You want to protect your loved ones from unexpected funeral expenses, medical bills, and unpaid debts without adding financial stress during their time of grief. Understanding key options like guaranteed issue life insurance, term policies, and permanent coverage is essential to making the best choice for your unique situation. At LD Financial Services, we specialize in offering compassionate and transparent insurance solutions designed to provide quick approval and fixed premiums, ensuring peace of mind for you and your family.

Take control of your legacy today by exploring reliable insurance options tailored for seniors and middle-aged adults planning ahead. Visit our site LD Financial Services to learn more about simplified application processes and affordable coverage. Don’t wait until it is too late. Book an appointment with a licensed agent now and secure the financial protection your family deserves.

Frequently Asked Questions

What is end-of-life insurance?

End-of-life insurance is a specialized financial product designed to provide monetary support to beneficiaries to cover immediate post-death expenses, such as funeral costs, outstanding medical bills, and personal debts.

How does guaranteed issue insurance differ from term and permanent life insurance?

Guaranteed issue insurance provides immediate coverage without medical examinations, making it accessible to those with health challenges, albeit at higher premiums and lower coverage amounts. In contrast, term life insurance offers coverage for a specific timeframe and requires health evaluations, while permanent life insurance provides lifelong coverage with cash value accumulation.

What are the eligibility requirements for end-of-life insurance policies?

Eligibility varies by policy type. Guaranteed issue policies typically require only basic personal information and age verification, while term and permanent life insurance require detailed health questionnaires and possibly medical examinations to assess risk and determine premiums.

What common mistakes should I avoid when selecting an end-of-life insurance policy?

Common mistakes include underestimating the necessary coverage amounts, overlooking critical policy details and exclusions, and choosing policies based solely on price without considering long-term financial implications. It’s essential to thoroughly evaluate policy terms and long-term costs.

Recommended