.png)

How to Get Life Insurance With Health Issues Easily

- Lincoln De Freitas

- Dec 19, 2025

- 8 min read

Every American family wants to make sure their loved ones are protected, but getting life insurance with health challenges can feel like a maze. More than 30 percent of American adults face medical conditions that complicate insurance approval. The process requires more than just filling out forms—it starts with gathering the right documents and knowing what insurers look for. Understanding each step can save time, reduce stress, and help you secure the coverage you need most.

Table of Contents

Quick Summary

Key Insight | Explanation |

1. Gather Comprehensive Documents | Collect detailed medical and financial records to support your application. |

2. Understand Policy Options | Explore different life insurance policies suitable for health conditions. |

3. Compare Multiple Insurers | Request quotes from several insurers to evaluate coverage and premiums. |

4. Consult Licensed Agents | Work with experienced agents for tailored advice based on your health. |

5. Review Policies Thoroughly | Examine coverage details carefully before accepting any insurance offer. |

Step 1: Gather Essential Health and Financial Documents

Getting life insurance with health challenges starts with organizing your critical paperwork. You will compile all necessary medical and financial records that insurance providers need to evaluate your application accurately.

Start by collecting comprehensive medical documentation that provides a clear picture of your health history. This means gathering medical records from all healthcare providers you have seen in the past 5-10 years. Request complete copies of your medical files, including diagnostic test results, treatment summaries, hospital discharge papers, and detailed physician notes about any chronic conditions. When preparing these documents, focus on providing comprehensive and honest medical information during the life insurance application process, as incomplete or inaccurate records can potentially lead to claim denials.

In addition to medical documents, compile financial records that demonstrate your current financial standing. These should include recent tax returns, pay stubs, bank statements, retirement account summaries, and any existing life insurance policies. Insurance companies will review these documents to assess your financial stability and determine appropriate coverage levels. Organize these papers chronologically and make clean, legible copies to streamline the application process.

Here is a quick summary of key documents needed for a successful life insurance application:

Document Type | Purpose for Insurer | Best Practice for Applicants |

Medical Records | Assess medical history | Obtain records from all providers |

Tax Returns | Verify financial stability | Gather at least two recent years |

Pay Stubs | Confirm income level | Use latest two pay periods |

Bank Statements | Review asset management | Provide 3-6 months of records |

Existing Policies | Check prior insurance coverages | Include all active and lapsed policies |

Pro Tip: Create a dedicated folder or digital file specifically for your insurance application documents. This ensures everything stays organized, easily accessible, and reduces stress during the application process.

Step 2: Evaluate Suitable Policy Types for Health Conditions

Navigating life insurance with existing health conditions requires understanding the various policy types available to you. Your goal is to find a coverage option that provides protection while accommodating your unique medical background.

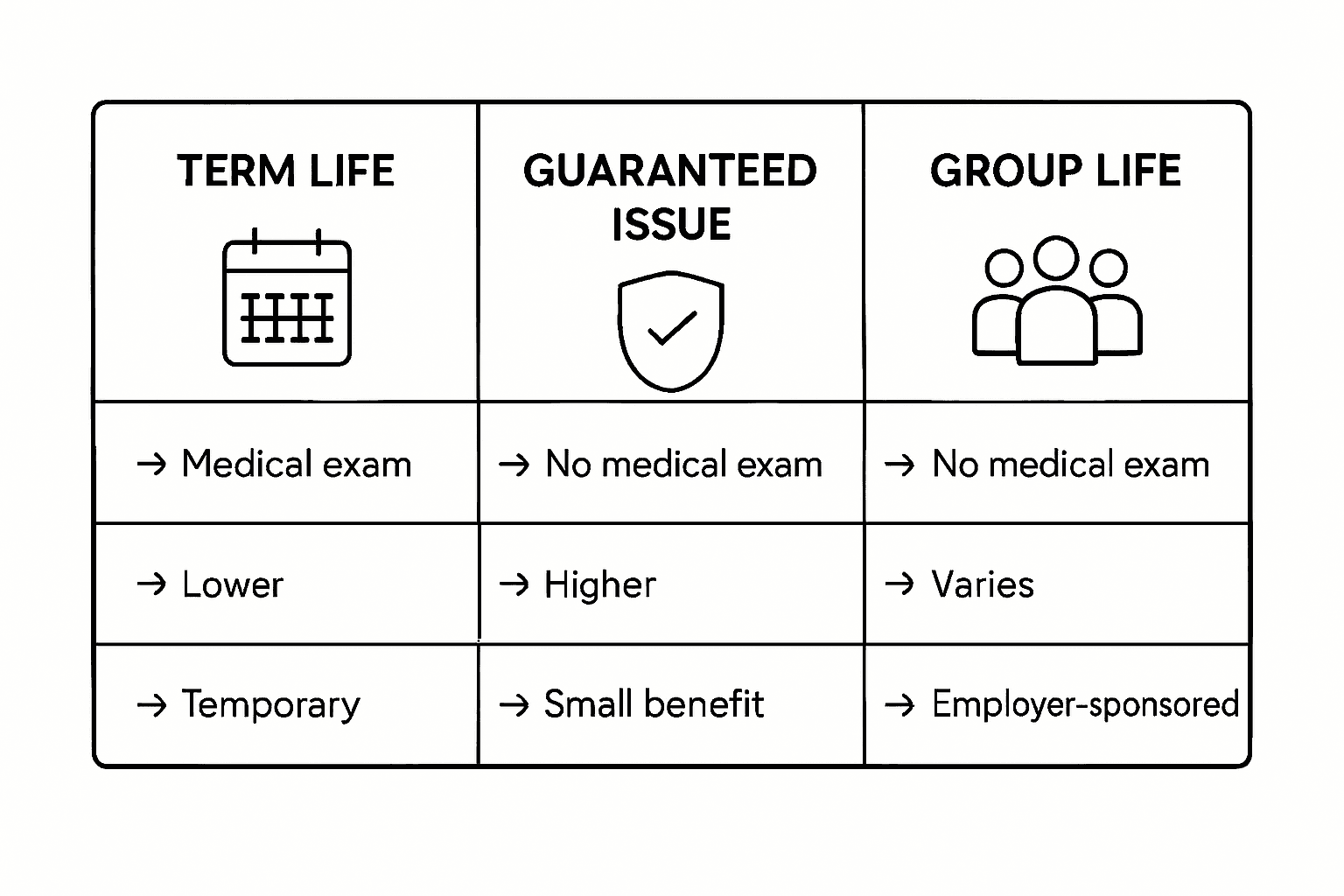

Individuals with pre-existing conditions have several life insurance options, including term life, guaranteed issue, group life, and whole life insurance policies. Each type offers distinct advantages depending on your specific health situation. Term life insurance typically provides coverage for a set period and might be more challenging to obtain with significant health issues. Guaranteed issue policies offer an alternative route with no medical exam required, though they often come with higher premiums and lower coverage amounts. Group life insurance through an employer can be more accessible, potentially offering coverage without extensive medical screening.

When evaluating these options, consider factors like your current health status, age, financial goals, and budget. Some policies might have waiting periods or specific restrictions for individuals with pre-existing conditions. While having a medical issue doesn’t automatically disqualify you from buying life insurance, it may result in fewer choices and higher costs, so thorough research and comparison are crucial.

This table compares popular life insurance policies for people with health challenges:

Policy Type | Medical Requirements | Typical Premiums | Coverage Features |

Term Life | Full underwriting | Moderate to high | Fixed term, large amounts |

Guaranteed Issue | No medical exam needed | High | Low coverage, limited payout |

Group Life | Minimal medical screening | Employer subsidized | Basic, often limited options |

Whole Life | Detailed underwriting | Highest cost | Lifetime, cash value builds |

Pro Tip: Schedule consultations with multiple insurance agents who specialize in high-risk or medically complex cases to get a comprehensive understanding of your best coverage options.

Step 3: Compare Plans From Trusted Insurers

Comparing life insurance plans becomes crucial when you have health challenges. Your objective is to find comprehensive coverage that meets your specific needs while navigating potential medical restrictions.

Securing life insurance with pre-existing medical conditions requires careful plan comparison, as each insurer evaluates health risks differently. Start by requesting quotes from at least three to five reputable insurance providers who specialize in high-risk or medically complex applications. Pay close attention to details like premium rates, coverage limits, waiting periods, and specific policy exclusions related to your health conditions.

When reviewing potential plans, create a comprehensive comparison spreadsheet that tracks key factors such as monthly premiums, total coverage amount, medical underwriting requirements, and any riders or additional benefits. Some insurers offer more flexible terms for specific health conditions, so thorough research can help you identify the most favorable options. Look for insurers with experience handling applications similar to your medical profile, as they will likely have more nuanced underwriting processes that could work in your favor.

Pro Tip: Request a detailed written explanation of how each insurer specifically evaluates your medical condition to understand potential coverage variations and make the most informed decision.

Step 4: Consult With Licensed Agents for Personalized Advice

Seeking personalized guidance through professional insurance agents can significantly improve your chances of finding suitable life insurance coverage. Your goal is to leverage expert knowledge tailored to your specific health circumstances.

Working with specialized insurance brokers experienced in high-risk cases can improve your chances of securing life insurance by connecting you with insurers more likely to understand and approve your unique medical background. During your consultation, prepare a comprehensive list of questions about how different insurers evaluate your specific health condition. Ask about their experience with similar medical profiles, potential underwriting strategies, and which companies have more flexible guidelines for your particular situation.

When meeting with licensed agents, bring all your medical documentation and be transparent about your health history. Experienced agents can help you navigate complex underwriting processes, identify insurers with more lenient policies, and potentially find coverage options you might not have discovered independently. They can also provide insights into strategies for improving your application’s approval odds, such as demonstrating ongoing medical management or highlighting positive health indicators.

Pro Tip: Request that the agent provide written recommendations comparing at least three potential insurance strategies specifically tailored to your medical profile.

Step 5: Apply and Review Coverage Confirmation Carefully

Submitting your life insurance application marks a critical moment in securing financial protection for your loved ones. Your focus now shifts to understanding and carefully evaluating the details of your potential coverage.

After applying for life insurance, it’s crucial to review the offered coverage thoroughly, as insurers may offer coverage on standard terms, rated terms, or potentially decline coverage based on your medical history. Carefully examine every aspect of the policy confirmation, paying close attention to premium rates, specific coverage limits, any medical exclusions, and potential rating adjustments that might impact your overall protection.

Understanding how specific health conditions affect life insurance premiums is essential for making an informed decision. Scrutinize the policy details for any clauses related to your pre-existing conditions, waiting periods, or special terms that might affect future claims. If any part of the coverage seems unclear or potentially restrictive, do not hesitate to request a detailed explanation from your insurance agent. Compare the final offer against the initial quotes and discussions you had during the consultation process to ensure all your expectations and needs are met.

Pro Tip: Have a trusted family member or financial advisor review the policy documents with you to catch any nuanced details you might have overlooked.

Secure Life Insurance Even With Health Challenges

Facing health issues can make finding the right life insurance feel overwhelming. This article shows that gathering detailed medical records and exploring options like guaranteed issue or term life insurance are key steps to overcoming barriers. At LD Financial Services, we understand how important it is to protect your family from unexpected final expenses without complicated hurdles or lengthy approvals.

You deserve compassionate and affordable coverage tailored to your unique health situation. Whether you are exploring simplified applications or need guidance on policies that accept existing medical conditions, our licensed agents are ready to help you every step of the way.

Take control of your future today with trusted end-of-life insurance solutions designed for people facing health challenges. Visit LD Financial Services now to schedule your free consultation. Discover how easy getting life insurance can be when you have expert support focused on transparency, quick approval, and fixed premiums. Start protecting your legacy and loved ones with confidence.

Frequently Asked Questions

How can I gather the necessary documents for life insurance with health issues?

Start by compiling all essential medical and financial records, including medical files from the last 5-10 years, tax returns, pay stubs, and bank statements. Organize these documents in a folder to ensure easy access when applying for insurance.

What types of life insurance are available for individuals with pre-existing health conditions?

Individuals with health challenges can consider various policy types, including term life, guaranteed issue, group life, and whole life insurance. Evaluate your health status and financial goals to determine which option may best meet your needs.

How can I effectively compare life insurance plans when I have health issues?

Request quotes from multiple reputable insurance providers and create a comparison spreadsheet that tracks premium rates, coverage limits, and specific medical underwriting requirements. This detailed approach will help you identify the most favorable plans available.

Should I consult an insurance agent, and how can they help me with my application?

Yes, consulting a licensed insurance agent can provide you with personalized guidance tailored to your health circumstances. Prepare a list of questions for the agent and bring your medical documents to ensure they assist you thoroughly during the application process.

What should I do if the life insurance policy offered has restrictions due to my health?

Carefully review the policy details, paying close attention to any exclusions or specific terms related to your health conditions. If you have concerns or find any part unclear, ask your insurance agent for a detailed explanation to understand your coverage fully.

Is it possible to get affordable life insurance if I have serious medical issues?

While securing affordable coverage can be challenging, it is indeed possible. Research various insurers, compare multiple quotes, and discuss your medical history candidly with agents to discover options that may offer competitive rates tailored to your situation.

Recommended

Comments