.png)

What Is Whole Life Insurance and Why It Matters

- Lincoln De Freitas

- Jan 1

- 8 min read

Most Canadian families know that planning for the future is more than just a financial decision. With rising final expenses and unpredictable life events, securing lasting protection becomes essential. Unlike typical american insurance models that end after a period, whole life insurance offers permanent coverage and a growing cash value. This guide breaks down how these policies work, helps you compare options, and highlights strategies to give your loved ones true peace of mind. Nearly 60 percent of Canadians cite estate planning as their top financial concern.

Table of Contents

Key Takeaways

Point | Details |

Whole Life Insurance Provides Lifelong Coverage | Whole life insurance lasts for your entire lifetime, as long as premiums are consistently paid, ensuring financial security for beneficiaries. |

Cash Value Accumulation Offers Additional Benefits | The policy builds a cash value component that grows on a tax-deferred basis, available for loans or withdrawals during the policyholder’s lifetime. |

Different Policy Types Cater to Varied Needs | Various whole life policy types, such as Traditional and Participating, offer tailored financial advantages based on individual circumstances. |

Consult Professionals for Informed Decisions | It is advisable to engage with financial and insurance advisors to maximize the benefits and navigate potential risks associated with whole life insurance. |

Whole life insurance basics explained

Whole life insurance is a comprehensive financial protection strategy designed to provide lifelong coverage and financial security for your loved ones. Unlike term life insurance that expires after a set period, whole life insurance remains in force for your entire lifetime as long as premiums are consistently paid.

The core characteristic of whole life insurance is its dual-purpose design. First, it guarantees a tax-free death benefit to your beneficiaries upon your passing. Second, it builds a cash value component that grows over time on a tax-deferred basis. This unique feature allows policyholders to accumulate savings they can potentially access during their lifetime through policy loans or withdrawals.

Key features of whole life insurance include:

Fixed, level premiums that do not increase with age

Guaranteed death benefit protection

Cash value accumulation that grows tax-deferred

Ability to borrow against the policy’s cash value

Permanent coverage that does not expire

Pro tip: Consider consulting a financial advisor to determine how whole life insurance can be strategically integrated into your comprehensive retirement and estate planning strategy.

Types of whole life policies compared

Whole life insurance offers several specialized policy types designed to meet diverse financial needs and personal circumstances. Understanding these variations can help Canadian families select the most appropriate coverage for their unique situation.

Traditional whole life policies provide consistent, lifelong protection with fixed premiums and a guaranteed death benefit. Participating whole life policies offer an additional attractive feature: the potential to earn annual dividends from the insurance company’s profits. These dividends can be used to reduce premiums, purchase additional coverage, or accumulate as cash value within the policy.

Key types of whole life insurance include:

Traditional Whole Life: Standard policy with fixed premiums and guaranteed benefits

Participating Whole Life: Offers potential dividend earnings

Limited Payment Whole Life: Allows complete premium payment within a shorter timeframe

Single Premium Whole Life: Requires one substantial upfront payment

Modified Whole Life: Provides lower initial premiums that increase over time

Each policy type carries distinct advantages, making it crucial to carefully evaluate your long-term financial goals and current economic situation before selecting a specific whole life insurance strategy.

Here’s a concise comparison to help you choose between popular whole life policy types:

Policy Type | Payment Structure | Unique Benefit |

Traditional Whole Life | Fixed premiums for life | Steady, lifelong protection |

Participating Whole Life | Regular or single payment | Dividend earnings potential |

Limited Payment Whole Life | Pay off over set years | No premiums after fixed period |

Single Premium Whole Life | One large upfront payment | Immediate, paid-up coverage |

Modified Whole Life | Low early, higher later | Flexible initial affordability |

Pro tip: Schedule a consultation with a licensed insurance professional to thoroughly assess which whole life policy type aligns most closely with your personal financial planning objectives.

How cash value and premiums work

Whole life insurance operates on a sophisticated financial mechanism that distinguishes it from other insurance products. Premiums are strategically divided between insurance coverage and cash value accumulation, creating a unique financial instrument that provides both protection and potential savings.

The cash value component grows gradually through a combination of fixed premium payments and tax-deferred interest. As you continue paying premiums, a portion is allocated to maintaining your insurance protection, while another portion is invested, generating potential returns. This accumulated cash value becomes an accessible financial resource that policyholders can leverage through policy loans or partial withdrawals, though such actions may reduce the overall death benefit.

Key aspects of cash value and premium structures include:

Consistent, level premium payments

Guaranteed minimum growth rate for cash value

Potential for additional dividends in participating policies

Tax-deferred growth of accumulated funds

Ability to borrow against accumulated cash value

Understanding the intricate balance between insurance protection and financial growth is crucial for making informed decisions about your long-term financial planning strategy.

Pro tip: Consult with a financial advisor to develop a comprehensive strategy for maximizing the potential of your whole life insurance policy’s cash value component.

Costs, taxes, and financial obligations

Whole life insurance involves complex financial considerations that extend beyond simple premium payments. Tax implications and financial obligations play a crucial role in understanding the true value of these policies, requiring careful planning and strategic decision-making.

The financial landscape of whole life insurance includes several key tax considerations. Death benefits typically remain tax-free for beneficiaries, providing a significant financial advantage. However, policyholders must navigate potential tax consequences when accessing cash value. Withdrawals exceeding the total premiums paid may trigger ordinary income tax, and early policy surrenders can result in unexpected tax liabilities.

Important financial aspects to consider include:

Higher premium costs compared to term life insurance

Fixed premium rates throughout the policy’s lifetime

Tax-free death benefits for beneficiaries

Potential tax implications for cash value withdrawals

Possible use in estate planning tax strategies

Policy loans that may impact overall financial obligations

Understanding the intricate balance between costs, tax implications, and long-term financial planning is essential for making informed decisions about whole life insurance investments.

Use this summary to understand how costs and taxes influence whole life insurance decisions:

Financial Aspect | Why It Matters | Possible Impact |

Premium Affordability | Affects monthly budget | May strain finances long term |

Cash Value Withdrawals | May trigger tax consequences | Reduces policy value |

Policy Loans | Creates repayment obligation | Lowers death benefit if unpaid |

Estate Planning | Can reduce taxable estate value | Enhances wealth transfer |

Pro tip: Consult with a certified tax professional and financial advisor to develop a comprehensive strategy that maximizes the tax advantages and minimizes potential financial risks associated with whole life insurance.

Common misconceptions and policy risks

Whole life insurance is often misunderstood, with many potential policyholders harboring misconceptions that can lead to poor financial decisions. Understanding the nuanced risks and realities of these policies is crucial for making informed choices about long-term financial protection.

Many individuals mistakenly believe that whole life insurance is always the most expensive or least flexible option. In reality, these policies offer unique financial advantages, including guaranteed death benefits, cash value accumulation, and potential dividend payments. However, they do come with potential risks such as high initial premiums, complex fee structures, and potential tax implications if not managed carefully.

Common misconceptions and associated risks include:

Believing whole life insurance is always too expensive

Assuming cash value grows quickly and without limitations

Misunderstanding the impact of policy loans on death benefits

Overlooking the long-term commitment required

Thinking the policy can be easily canceled without financial penalties

Underestimating the complexity of policy management

Navigating the intricate landscape of whole life insurance requires careful research, professional guidance, and a realistic understanding of both the potential benefits and inherent risks.

Pro tip: Request a comprehensive policy illustration and have a licensed financial advisor walk you through the potential scenarios and long-term implications before making a final decision.

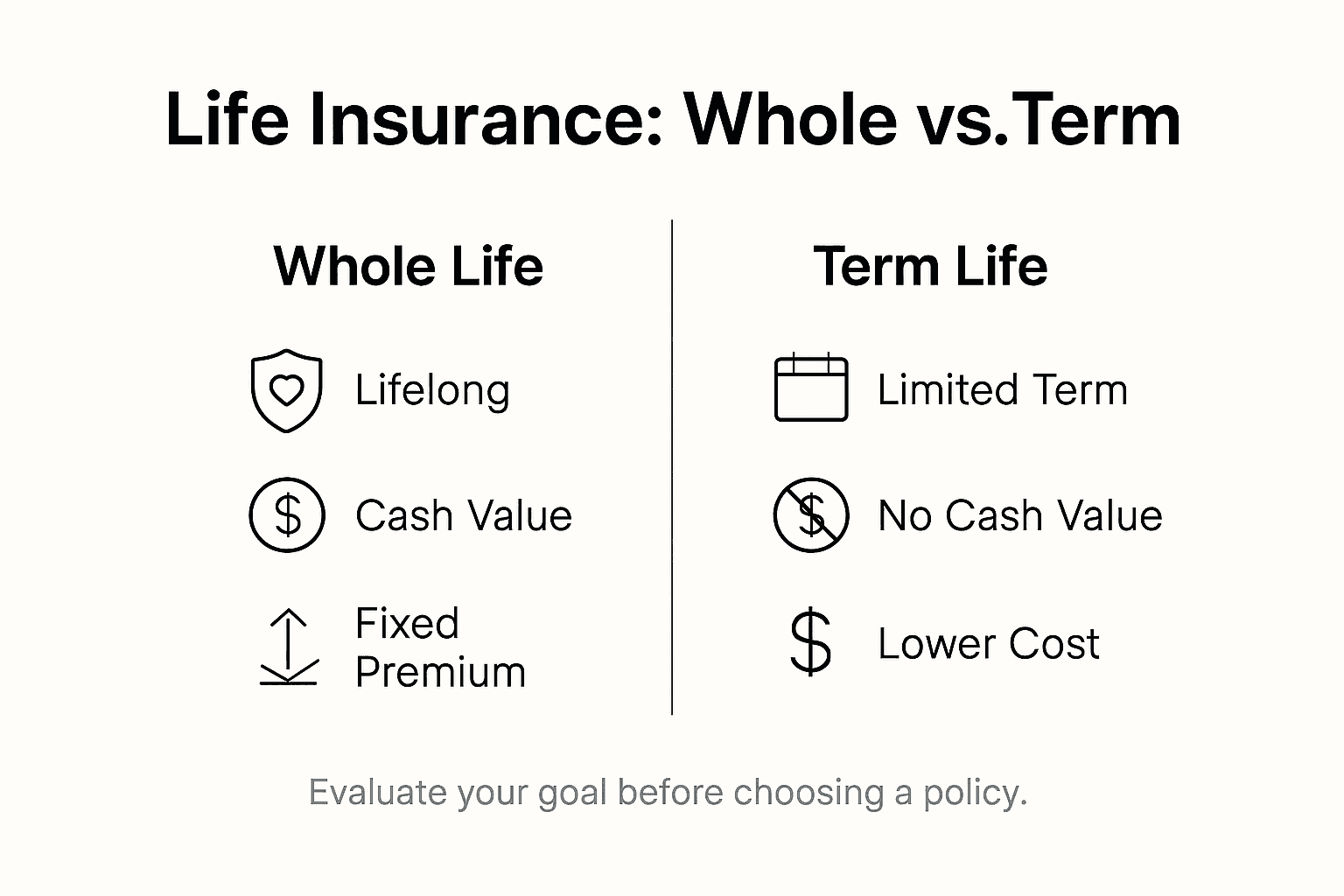

Whole life vs. term life in Canada

Life insurance choices in Canada require careful consideration of individual financial circumstances and long-term goals. The fundamental differences between whole life and term life insurance can significantly impact your financial planning strategy, making it crucial to understand their distinct characteristics.

Term life insurance offers a straightforward approach with lower initial premiums, typically covering specific periods like 10, 20, or 30 years. These policies are ideal for Canadians seeking temporary financial protection, such as covering mortgage obligations or supporting young families during critical earning years. Whole life insurance, by contrast, provides lifelong coverage with a guaranteed death benefit and a cash value component that grows tax-deferred, making it more suitable for comprehensive estate planning and long-term financial security.

Key comparison points include:

Premium Costs: Term life has significantly lower initial premiums

Coverage Duration: Term life expires after set period; whole life covers entire lifetime

Cash Value: Whole life builds cash value; term life does not

Financial Flexibility: Whole life offers policy loans and cash value access

Estate Planning: Whole life provides permanent financial protection

Investment Component: Whole life includes potential dividend earnings

Choosing between term and whole life insurance depends on your specific financial objectives, age, family situation, and long-term economic goals.

Pro tip: Schedule consultations with multiple insurance professionals to receive personalized comparisons that align with your unique financial circumstances and future planning needs.

Protect Your Legacy with Trusted Whole Life Insurance Solutions

Understanding whole life insurance is the first step toward securing lifelong financial protection for your loved ones and ensuring peace of mind around the costs that matter most. If you are concerned about fixed premiums, cash value growth, and ensuring a reliable death benefit, LD Financial Services specializes in helping middle-aged and senior adults like you navigate these complexities with compassionate guidance.

Explore affordable and transparent insurance options tailored for final expenses including funerals, medical bills, and outstanding debts. Take control of your estate planning today by speaking with licensed agents who make securing permanent coverage straightforward. Visit LD Financial Services to learn how whole life insurance can protect your family’s financial future. Get started now with a simplified application and quick approval to ensure your legacy is well protected.

Frequently Asked Questions

What is whole life insurance?

Whole life insurance is a type of permanent life insurance that provides lifelong coverage as long as premiums are paid. It offers a guaranteed death benefit to beneficiaries and includes a cash value component that grows tax-deferred over time.

How do whole life insurance premiums work?

Whole life insurance premiums are fixed and level, meaning they do not increase with age. A portion of each premium contributes to the insurance coverage, while another portion accumulates cash value over time.

What are the benefits of whole life insurance compared to term life insurance?

Whole life insurance offers lifelong coverage, a guaranteed death benefit, and a cash value component that grows over time, while term life insurance provides temporary coverage at lower initial costs but does not accumulate cash value.

Can I access the cash value in my whole life insurance policy?

Yes, policyholders can access the cash value through policy loans or withdrawals, though it’s important to consider that this may reduce the overall death benefit and could have tax implications.

Recommended